SEIS (Seed Enterprise Investment Scheme) and EIS (Enterprise Investment Scheme) are like helpful tools from the UK government that make it easier for you to persuade investors to invest their money in your business.

Facebook

Twitter

LinkedIn

Pinterest

Pocket

WhatsApp

How do SEIS/EIS benefit investors?

SEIS/EIS is like a safety net for investors when they support your startup financially. It doesn’t directly benefit your startup, but it makes investors more comfortable with the idea of investing in it. This is a significant advantage, and many investors may inquire right away if your startup qualifies for SEIS/EIS.

Make sure to inform potential investors that you have obtained SEIS/EIS Advance Assurance from HMRC. We can assist you in obtaining this assurance at no cost.

In simple terms:

- EIS (Enterprise Investment Scheme): Investors can receive a tax reduction of 30% on their investment, up to £2,000,000 per year, and they also enjoy an exemption from Capital Gains Tax.

- SEIS (Seed Enterprise Investment Scheme): Investors can get a tax reduction of 50% on their investment, up to £200,000, and they also benefit from a Capital Gains Tax exemption.

If your startup unfortunately fails and is shut down, investors can receive relief for their losses from HMRC. This relief can range from 22.5% to 31.5% of their initial investment, providing some financial support in case things don’t go as planned.

You can provide a single investor with both SEIS and EIS benefits for their investment. This is known as a SEIS/EIS dual raise, and it allows the investor to enjoy the advantages of both schemes.

Starting a new business can be tough, especially because one of the biggest challenges is convincing investors to believe in your vision, just like you did when you decided to become a founder.

SEIS (Seed Enterprise Investment Scheme) and EIS (Enterprise Investment Scheme) are like government programs that make it easier for you to persuade investors to invest their money in your business.

These schemes were created to inspire investors to contribute more funds to risky startups by offering them tax benefits that essentially lower the overall cost of their investment. This tax benefit works as a reduction in the amount of income tax the investor needs to pay personally.

In addition, if your startup achieves incredible success and is acquired for a substantial amount after potentially solving world hunger (fingers crossed!), investors also receive a special benefit: they won’t have to pay Capital Gains Tax on the profits they make from the sale. More information on how this benefit works for your investors can be found below.

In short, if you give your investors an SEIS/EIS certificate, they’ll get most of their money back in the form of tax relief whether you succeed or fail. It’s a cheap benefit to offer investors if you qualify for SEIS/EIS (like most early-stage startups) and the only costs are the application and HMRC paperwork.

As mentioned, F6S helps many startup founder clients successfully complete the HMRC application with minimal work and for free.

We’ll cover applying for SEIS and/or EIS, pros and cons of each, and tips on setting up your startup for SEIS/EIS without getting distracted from your most important goal – growing your startup.

What is SEIS/EIS?

Let’s tackle them separately.

EIS – Need to Know

EIS stands for Enterprise Investment Scheme, and it was created to help small companies, including startups like yours, attract more investor funds when they sell shares.

HMRC views the EIS investment scheme as being specially designed to support high-risk companies, especially those that might face difficulties attracting investors on their own due to their newness and inherent risk. This scheme appears to be tailor-made for early-stage tech startups and similar ventures.

EIS operates by providing tax relief to your investors. When they invest in your startup, they not only receive shares in your company but also enjoy a reduction in their personal tax liability, courtesy of HM Revenue & Customs. In simpler terms, they pay less in taxes on the money they earn, which is almost like having extra money in their pockets.

Under the EIS, investors can invest up to £2 million per year in unlisted companies, which often includes startups. If at least £1 million of that investment goes into knowledge-intensive companies, it’s even more beneficial. However, it’s important to note that this investment must remain qualified for at least three years.

The exciting part is that investors can promptly claim up to 30% of their investment back from HMRC when they file their personal tax return. This means they can get a significant portion of their invested money back relatively quickly.

If your startup meets the criteria for EIS, you can raise a maximum of £5 million per year through this scheme. However, there is also a cumulative limit over the total life of your startup, which means you can raise up to £12 million in EIS-eligible investment throughout your startup’s existence. This limit helps ensure the scheme is primarily used by smaller businesses and startups.

How can you determine if your startup is eligible to provide EIS benefits to investors when they acquire your shares?

Chances are, you qualify for EIS if you:

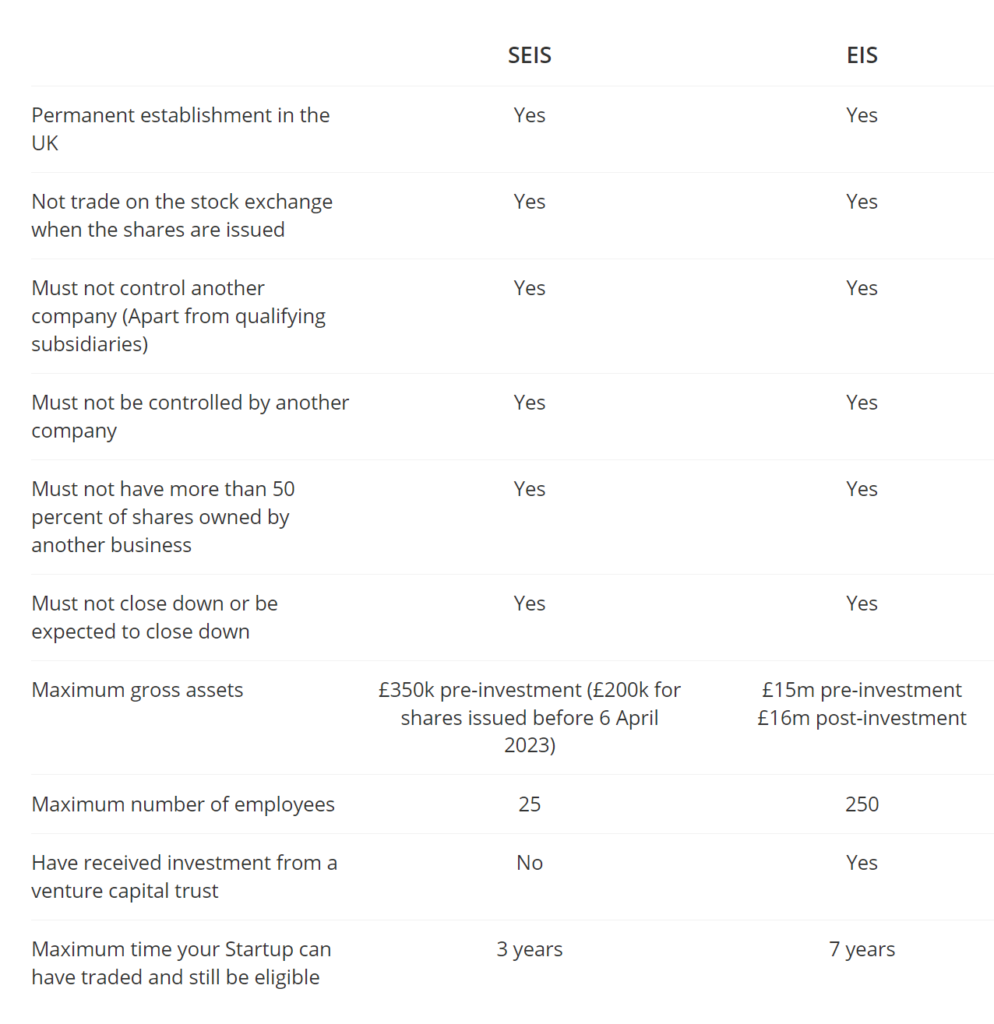

- Your company has a permanent establishment in the United Kingdom.

- Your company doesn’t control another company (though qualifying subsidiaries are acceptable).

- Your company doesn’t intend to shut down after completing a specific number of projects.

- Your company’s gross assets are below £15 million before issuing shares or below £16 million after shares are issued.

- Your company has fewer than 250 full-time employees.

According to HMRC, most trades are eligible for SEIS/EIS, but there are some excluded activities. You can refer to the checklist below to identify which trades are not eligible for SEIS/EIS benefits.

- Dealing in commodities/futures in shares, land, securities and any other financial instruments.

- Dealing in goods that don’t fall under trade/retail/wholesale distribution.

- Financial activities – hire-purchase financing, debt-factoring, money-lending, insurance, and banking.

- Letting/leasing assets on hire (ship-chartering trades not included in this category of exclusions).

- Sectors receiving licence fees and/or royalties.

- Providing accountancy/legal services.

- Property development.

- Market gardening/farming.

- Coal production.

- Steel production.

- Managing, occupying or holding woodlands (applies to the whole forestry/timber production sector).

- Shipbuilding.

- Managing or operating hotels.

- Exporting or generating electricity (this attracts the Feed in Tariff).

- Activities that involve providing services/facilities for another founder’s business in the event that his business’ activity falls under the categories we’ve listed.

SEIS – Need to know

The Seed Enterprise Investment Scheme (SEIS) is often considered one of the best options for early-stage founders.

In technical terms, SEIS operates similarly to EIS by providing tax reliefs to investors who purchase new shares in your company. According to HMRC rules, companies can benefit from up to £250,000 of SEIS relief for investors.

Investors who opt to purchase shares from your company can enjoy a generous 50% income tax relief on investments, up to a limit of £200,000. However, there are certain conditions that must be met.

For instance, your startup should not have more than 25 employees or gross assets exceeding £350,000 (£200,000 for shares issued before 6 April 2023) to qualify for SEIS. Additionally, your startup must not have been trading for more than 3 years to be eligible for SEIS benefits.

You’re likely to be eligible for SEIS if your startup:

- Carries out a new qualifying trade.

- Is established in the UK.

- Doesn’t have gross assets over £350,000 (£200,000 for shares issued before 6 April 2023).

- Isn’t in a partnership.

- Has 25 or less full-time employees when it issues shares.

What type of tech startups can get SEIS and/or EIS?

We’ve created a table to assist you in determining what’s most suitable for your startup. If you have any questions, please don’t hesitate to contact us for a free consultation.

When did your startup officially begin operating business?

The “start of trading” is a crucial factor for SEIS/EIS. It marks the beginning of a two-year period for EIS eligibility, and it also determines when your startup loses the ability to claim EIS relief entirely after seven years.

It’s important to note that your startup’s start of trading may not align with its incorporation date or when you initially began working on the project. According to HMRC, the start of trading is when you either make your startup’s first commercial sale or are ready to do so.

This can be a bit complex, but we’re here to offer free advice to ensure you comply with HMRC rules and make the most of SEIS/EIS opportunities.

Advance Assurance

It’s a smart move to check with HMRC to see if investors who purchase shares in your startup are eligible for SEIS and/or EIS relief on their investment. You can, and usually should, do this even before you secure investment, using a convenient process called ‘Advance Assurance.’

You have the option to handle Advance Assurance on your own, or you can turn to F6S for assistance. The primary advantage for your startup when obtaining Advance Assurance is that you can inform potential investors right away that HMRC has already approved your SEIS or EIS eligibility. However, it’s crucial to ensure that you continue to meet the qualifying criteria.

What advantages do SEIS and/or EIS offer to founders and startups?

Securing investment for your startup can be a challenging task for any founder, even when investors are receiving shares in your company in exchange.

Having your investment round approved as SEIS and/or EIS eligible provides investors with the assurance that they will receive at least 30% of their investment back immediately as a tax credit. The idea behind SEIS and/or EIS investor refunds is that they make investors more inclined to invest in your early-stage idea, which can ultimately benefit you and your startup.

How does SEIS and/or EIS benefit investors?

Investors receive a tax refund when they invest in your startup through SEIS/EIS. This goes beyond the income tax relief we discussed earlier. They also benefit from reduced taxes if they decide to sell their shares in your startup. This tax reduction is known as the Capital Gains Tax Exemption.

The Capital Gains Tax Exemption means that SEIS/EIS investors in your startup won’t have to pay taxes when they sell their EIS or SEIS shares. However, this tax benefit applies only if they hold their shares in your company for at least three years, and your startup continues to meet the qualifying criteria throughout the investment period.

Furthermore, SEIS/EIS investors are entitled to loss relief. In case your startup doesn’t succeed and you need to close it down, investors can receive a tax credit ranging from 22.5% to 31.5% of their investment, depending on their income tax rate.

What type of investors can get EIS/SEIS?

HMRC’s primary aim with EIS/SEIS is to attract external investors who are willing to invest in your company. Therefore, the rule is straightforward: anyone who is not closely associated with your company can invest money in your business through EIS/SEIS, provided they have tax liabilities in the UK.

However, there are certain types of investors who cannot avail EIS and/or SEIS relief when investing in your startup. For instance:

- Investors and their associates who collectively hold more than 30% of your company’s share capital.

- Relatives of individuals closely connected with your business (with the exception of siblings).

- Business partners of individuals closely connected with your company.

These restrictions are in place to ensure that the tax benefits of EIS/SEIS are primarily directed toward genuinely external investors.

How do you apply for SEIS and/or EIS?

We strongly advise startup founders to begin by obtaining Advance Assurance (AA). This is HMRC’s way of verifying that investors who buy shares in your startup can indeed benefit from the tax advantages of SEIS/EIS.

Remember that the validity of Advance Assurance relies on you submitting a comprehensive, accurate, and honest application, which should still hold true when the investment is made.

Here’s how you apply for Advanced Assurance:

Step 1: Ensure that you are the appropriate person within the startup to apply.

The director or secretary of your startup are the only individuals who can request Advanced Assurance or grant authorization for an application. Alternatively, you can engage an agent, like F6S, to handle the preparation, submission, and proper processing of the application.

We believe a reliable agent can efficiently gather the necessary information from you and construct a strong Advance Assurance application, allowing you to concentrate on attracting investors and nurturing your startup’s growth.

Step 2: Collect essential information for your application.

To persuade HMRC that investments in your startup are eligible for SEIS and/or EIS, you’ll need to provide them with specific information. Some of the information you’ll need to prepare includes:

- How much you think you’ll raise.

- Your startup’s financial forecasts.

- Your startup’s business plan.

- Your startup’s most recent accounts.

- Details on how your business will use the SEIS and/or EIS investment.

- Info about your ongoing trading and activities, and how much you plan to spend on each activity.

- Info about previous Venture Capital Trusts you enrolled into and how much you got from them.

- Latest memorandum/articles of association.

- Register of members, which must be from the date you apply for Advance Assurance.

- Latest documents you’ve used to explain business proposals to interested investors.

- Documents that detail agreements between your company and shareholders.

- A signed letter from a Director (if you want F6S to act on your behalf).

- Any document that you consider pertinent to SEIS and/or EIS.

- Details of at least one potential investor (recently added requirement).

Step 3: Complete the Advance Assurance application.

Visit HMRC’s online Advance Assurance application and fill in all the requested information. Upon completion, you’ll receive a copy of your application.

Step 4: Submit your application to HMRC.

You can do this by email, or if you prefer, we can handle it on your behalf.

Step 5: Await a response from HMRC.

HMRC typically takes four to five weeks to respond with Advance Assurance, confirming your eligibility for SEIS/EIS. This confirmation is often referred to as the ‘Golden Ticket,’ and it’s something potential investors will want to see.

Let’s get started on your SEIS and EIS applications.

Applying for EIS relief after receiving investment

Step 1: Fill out an EIS1 Compliance Statement.

Visit HMRC’s website and complete the EIS1 compliance statement.

Step 2: Submit the application to HMRC.

Download the completed form and send it to HMRC via email or through your agent.

Step 3: Obtain your SEIS/EIS Compliance Certificates.

Obtain your compliance certificates and the HMRC letter. Share the completed compliance certificates with your investors to demonstrate that the investment is EIS-compliant, allowing them to claim EIS relief and the associated benefits we’ve discussed.

Applying for SEIS relief after receiving investment

Step 1: Fill out a SEIS1 Compliance Statement.

Visit HMRC’s website and complete the SEIS1 compliance statement.

Step 2: Submit the application to HMRC.

Download the form to your computer and send it to HMRC via email or through your agent.

Step 3: Obtain compliance certificates from HMRC.

Receive your compliance certificates and the HMRC letter. Share the completed compliance certificates with your investors to confirm that the investment is SEIS-compliant, allowing them to claim SEIS relief.

Can you get SEIS and EIS in the same investment round?

Indeed, it is possible to obtain both SEIS (Seed Enterprise Investment Scheme) and EIS (Enterprise Investment Scheme) benefits in the same investment round, often referred to as an “SEIS/EIS dual raise.” Here’s how it typically works:

Sequential Investment:

SEIS shares are issued first as the “first completion” of the investment round.

Additional EIS Investment:

Once the SEIS investment is completed, the same investor can make an additional investment under EIS, known as the “second completion,” within the same investment round.

Sequential Fund Collection:

Funds raised for SEIS and EIS are collected sequentially. First, the SEIS portion is collected, and SEIS shares are issued. Then, the EIS portion is collected, and EIS shares are issued.

Separate Share Certificates:

As a result, the investor will have two separate share certificates issued on different dates, reflecting the SEIS and EIS investments made during the same round.

It’s important to note that SEIS must be used before EIS in the same investment round. Additionally, all legal and regulatory requirements for both SEIS and EIS must be met, and Advance Assurance should be obtained for both schemes to ensure eligibility.

This approach allows investors to benefit from both SEIS and EIS tax reliefs within a single investment round, offering a compelling incentive for them to support your startup.

What are the most common SEIS/EIS failures?

SEIS/EIS are fantastic programs, but getting the details right is crucial. Here are the four most common pitfalls and misconceptions we’ve encountered:

Getting the trading windows for SEIS/EIS wrong

Your startup must receive EIS investment within seven years of the first sale you make. For SEIS it must be within two years of beginning to trade

You issue shares before receiving the cash from investors

HMRC advises that you should have the money in your bank account before issuing shares. Always issue shares only after you receive the cash.

Advance Assurance just puts you on par with other startups – you still need to have a great idea, pitch and (preferably) traction

There are lots of founders and startups hustling for investor money. SEIS and EIS can reduce the risk for investors, but isn’t a guarantee of success. Most other good startup investments will also have Advance Assurance. You should think of Advance Assurance as the cost of playing the game and not as a success in itself.

Mistakes in paperwork delay Advance Assurance

Incomplete or missing paperwork can mean that you’ll have to start again. We see founders and startups that lose months due to simple mistakes or a lack of knowledge about what HMRC considers a complete Advance Assurance application.

SEIS and EIS are powerful tools that can significantly enhance your startup’s appeal to investors. While there’s a fair amount of paperwork involved, when done correctly and in the right order, the tax benefits your investors receive are well worth it.

Moreover, after securing investment, there are additional government tax credits, such as R&D Tax Credits, that can contribute to your startup’s financial health.

We’re here to assist and address any questions or concerns to ensure you successfully navigate the process of obtaining both SEIS/EIS and managing your investors.

Facebook

Twitter

LinkedIn

Pinterest

Pocket

WhatsApp

Never miss any important news. Subscribe to our newsletter.

Related News

Top 10 Winter Wellness Tips!

July 3, 2026

Explore York: 5 Heritage Pubs for History Buffs

July 3, 2026

The Impact of AI on Every Scientific Frontier

July 3, 2026

Burning Waste Becomes UK’s Dirtiest Energy Source

July 3, 2026

What causes autumn leaves to change their color?

July 3, 2026

Telephone’s Inventor: Who was it?

July 3, 2026